Australian Prudential and Regulation Authority (APRA) Chairman Wayne Byres recently discussed the results of APRA’s latest banking industry stress test conducted in 2017 whose results were not disclosed in detail previously. Under APRA’s stress test scenario, the thirteen largest domestic banks underwent a simulation involving a severe economic crisis in Australia and New Zealand caused by an economic collapse in China and a downfall in demand for commodities, combined with a “significant downturn in the housing market at the epicentre.” This hypothetical situation resulted in Australia’s GDP falling by 4%, the unemployment rate doubling to 11% (a level last seen in the 1991 recession in Australia) and domestic house prices dropping 35% over three years.

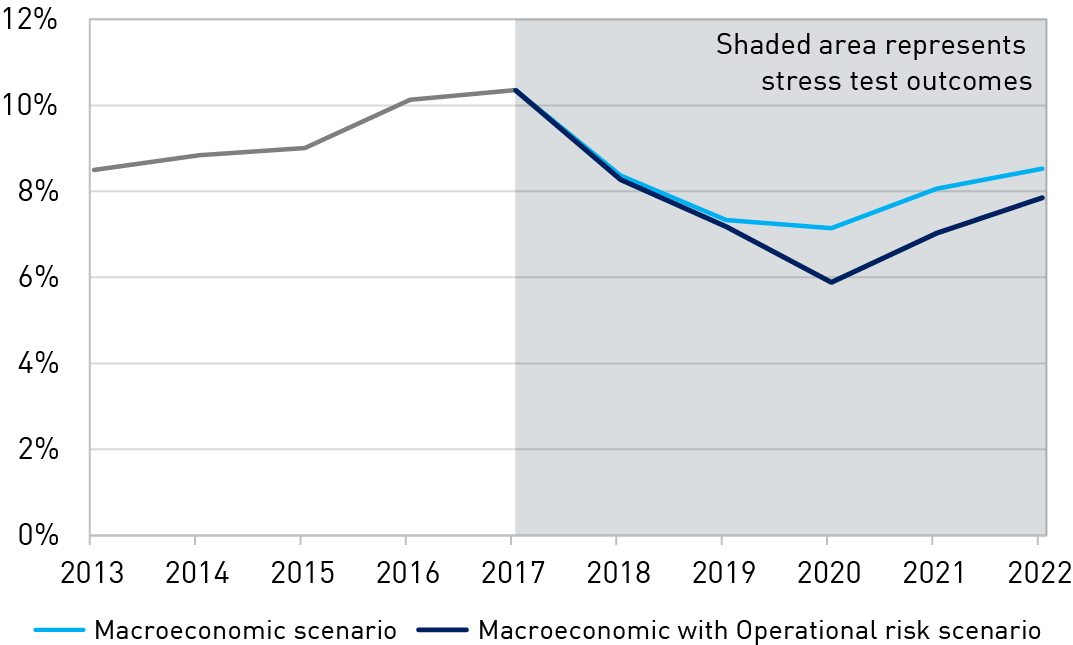

Under APRA’s stress test scenario, despite the significant credit losses incurred by the banks, their capital levels remained above the regulatory minimum levels throughout the hypothetical crisis. APRA reported “the common equity tier 1 (CET1) ratio of the industry fell from around 10.5 per cent at the start of the scenario to a little over 7 per cent by year three; a fall of more than 3 percentage points from peak to trough. This was driven by a combination of higher funding costs, significant credit losses and growth in risk weighted assets reflecting the deterioration in asset quality.”

CET1 Capital Ratio results – Macroeconomic and Operational Risk Scenario Source: APRA

Source: APRA

Another factor to consider is that in the above scenarios there was no compulsory write-down or conversion of bank hybrid or subordinated debt. As part of new regulation since the global financial crisis, these new instruments have been created to supplement banks’ capital ratios in times of crisis and provide additional protection to depositors (and senior debt holders). While it is questionable whether a bank could survive on a long term basis if it were to write-off its hybrid and subordinated debt, in the short term this mechanism would very likely ensure no losses for senior debt holders while the bank was either liquidated, restructured or more hopefully acquired by another bank.

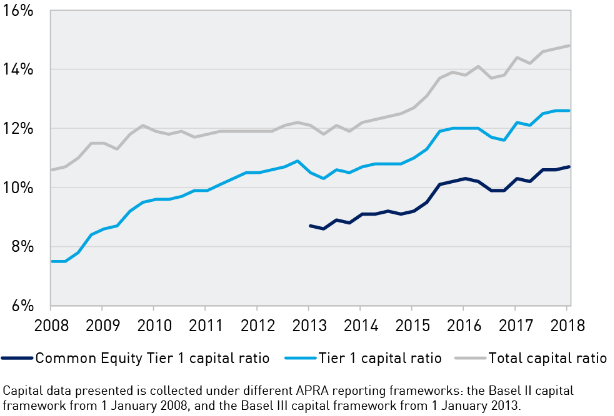

Amicus overall conclusion from this study is the Australian banking system appears very robust. As can be seen from the chart below, average capital was around 11% entering the 2008 global financial crisis which the Australian banks all survived with relatively minor impact and since then capital levels have risen to 15% making the banks even stronger today. This past experience of surviving the GFC is consistent with the banks also passing APRA’s latest stress test.

ADI Industry Capital Ratios

Source: APRA